Oman was the last GCC state to introduce Islamic banking, launching the sector by Royal Decree in December 2012. The Central Bank of Oman (CBO) regulates every Islamic bank and window, and issued Royal Decree 96/2012 to organise the Sharia-compliant products they may offer. Despite its late start, the sector grew quickly — this study examines the mechanism through which that financial system is being developed.

To Q1 2017: financing rose ~37% and deposits ~41% year-on-year (Central Bank of Oman statistical bulletin).

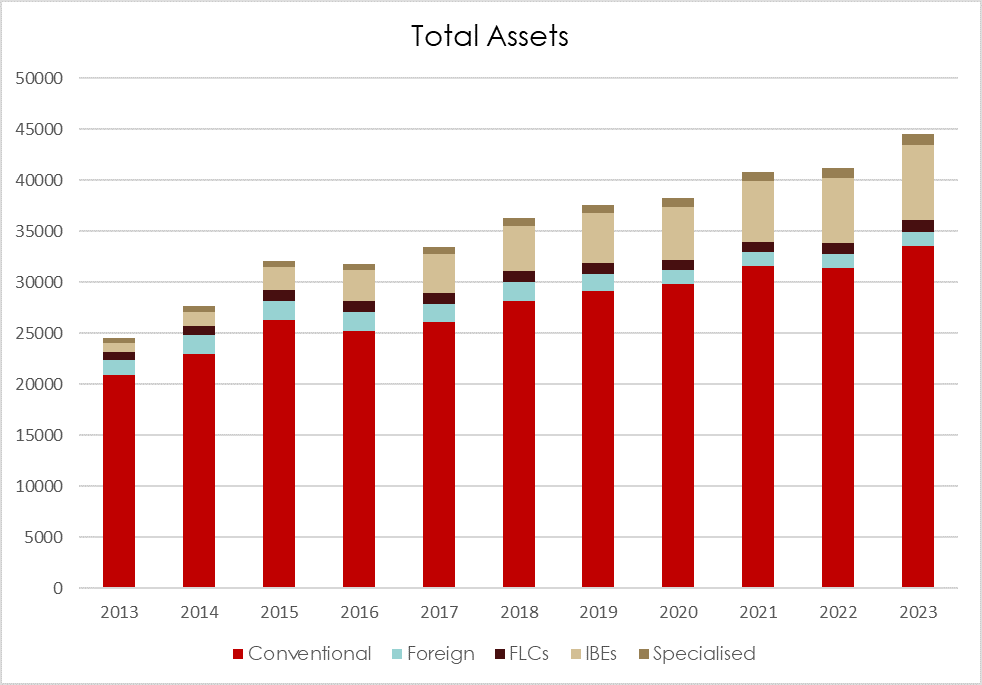

A decade of asset growth

Since the first licences, the assets of Oman's banking system have climbed steadily, with Islamic banking entities ("IBEs") capturing a widening share of the market.

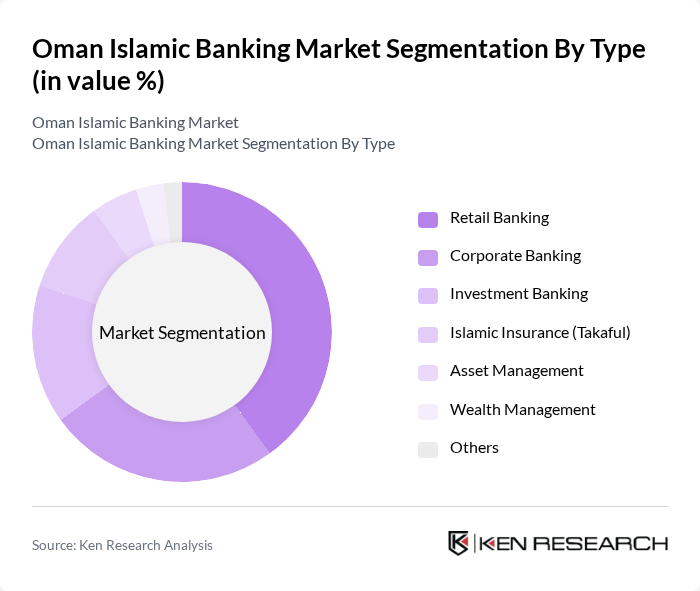

The market by type

Islamic banking is not monolithic: it spans retail and corporate banking, investment banking, Takaful (Islamic insurance), and asset and wealth management.

Why customers choose Islamic banking

Demand is driven heavily by faith. A survey by IFAAS found that the great majority of Omanis hold a conventional product — but most would prefer to avoid interest if a viable alternative exists.

The Sharia-compliant instruments

Under CBO supervision, Oman's Islamic banks replace interest with asset- and partnership-based structures:

- Murabaha & Musawama — cost-plus and negotiated-price sale financing

- Ijarah — leasing

- Mudaraba — profit-sharing investment

- Musharaka & Diminishing Musharaka — partnership financing

- Salam & Istisna — forward purchase and manufacturing finance

(The CBO no longer permits Tawaruq as a Sharia-compliant service in Oman.)

The banks and windows

The sector is served by full Islamic banks and by Islamic "windows" of conventional banks:

- Bank Nizwa — full Islamic bank (Jan 2013)

- Alizz Islamic Bank — full Islamic bank (Nov 2012, OMR 100m capital)

- Meethaq (Bank Muscat) — window that became a semi-independent bank in Dec 2016, with over OMR 2.7bn in assets

- Maisarah (Bank Dhofar) — window (2013)

- Muzn (National Bank of Oman) — Oman's first Islamic window (2013)

Challenges — and how to develop the sector

Growth is not guaranteed. The study identifies four main obstacles: slow, centralised product approval at the CBO; limited public awareness of Islamic banking; a shortage of professionally trained Islamic bankers (many recruited from conventional banks); and tough competition with established commercial banks. To address them, it recommends:

- More decentralised, flexible product approval from the CBO.

- Long-term marketing strategies targeting Omanis, expatriates, and international markets.

- Dedicated staff development — training, workshops, and a national conference on Islamic banking.

- Competitive profit margins, and building Islamic-finance talent through universities and field training.

In barely a decade, Islamic finance in Oman moved from a policy decision to a structural part of the financial system — but its next phase depends on awareness, talent, and a lighter regulatory touch.

Conclusion

Oman's Islamic banking story is one of disciplined, regulator-led growth, closely tied to the wider economy and to government funding. Building a strong, sustainable financial system rests on economic diversification — the central ambition of Oman's national vision — and on continued investment in products, liquidity, and people.

Source: Mohammed Ahmed, M. B., & Al-Sarhani, Y. A. (2018). Developing Mechanism of Financial System for Islamic Banks in Sultanate of Oman. International Journal of Engineering Researches and Management Studies (IJERMS), 5(2). Asset-growth and segmentation figures supplied by Knowledge Investment. This article is an editorial summary of the published paper.